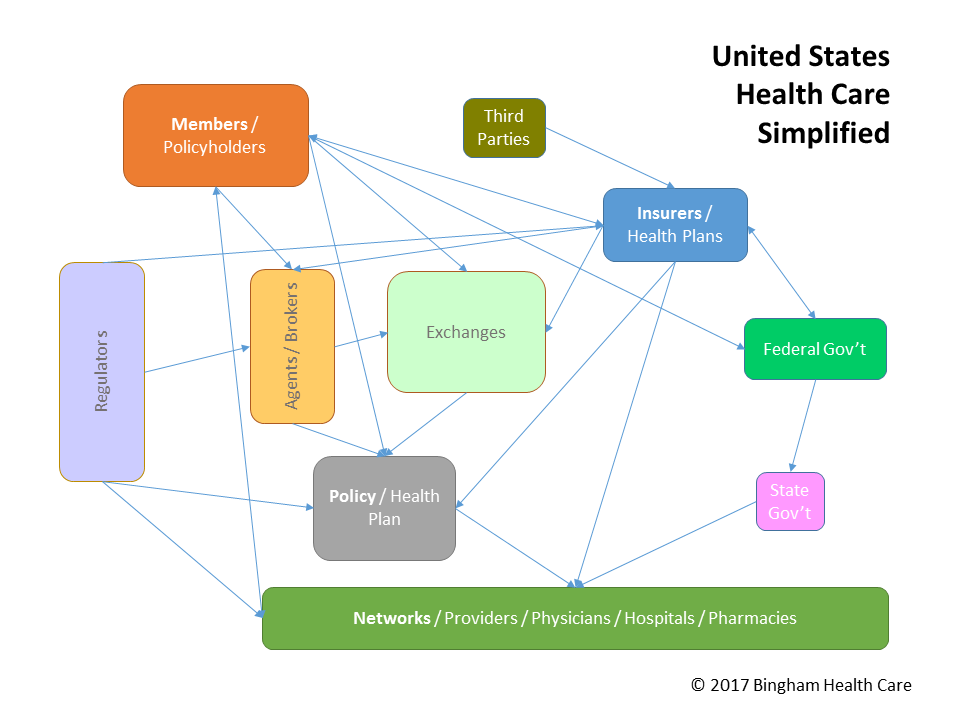

To understand healthcare, as they say: follow the money. At its center is the healtcare product, or policy. Like many businesses, providing healthcare coverage requires creating a desirable product, pricing it appropriately, marketing it well, getting it in consumers hands, and then ensuring that using the product meets or exceeds consumer expectations, hopefully generating repeat and expanded business.

The healthcare product is a policy. Rather than just purchasing the policy one time, eligible buyers schedule a recurring payment plan that auto-renews, buyng the policy monthly, each time giving the member(s) coverage for the subsequent month. For example, someone might sign-up for coverage in January, make an initial payment, and be covered under the policy for the month of February. Then, before the end of February, the consumer would make another monthly payment, extending the policy's coverage through March. This continues until the policy ends by its own terms, the consumer decides to not pay for more coverage, or the issuer (i.e., the insurance company or other business that sells the policy) finds reason to terminate coverage.

Of note here is that while the payments "renew" every month, extending the policy's coverage, the policy does not renew each month. Rather, healthcare policies often have a 1-year or calendar-year term, and may end, renew, or become renewable at the end of 12 months or at the end of the calendar year.

In exchange for the buyer's payment, known as a premium, the policy provides one or more people, called members, healthcare coverage. These members are able to get health care services and products from healthcare providers. What is special is that, without being on the policy, a person might not be able to get care from some of the providers, and even for the other providers, obtaining care through the policy often results in lower member costs than the member would otherwise have to pay, if they saw the providers sans policy.

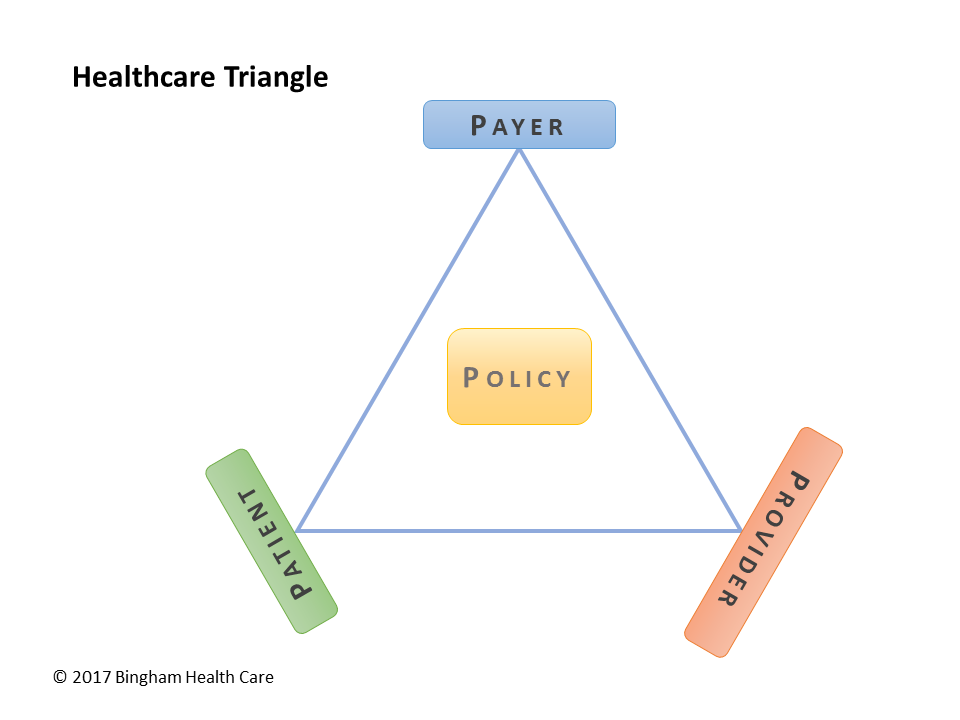

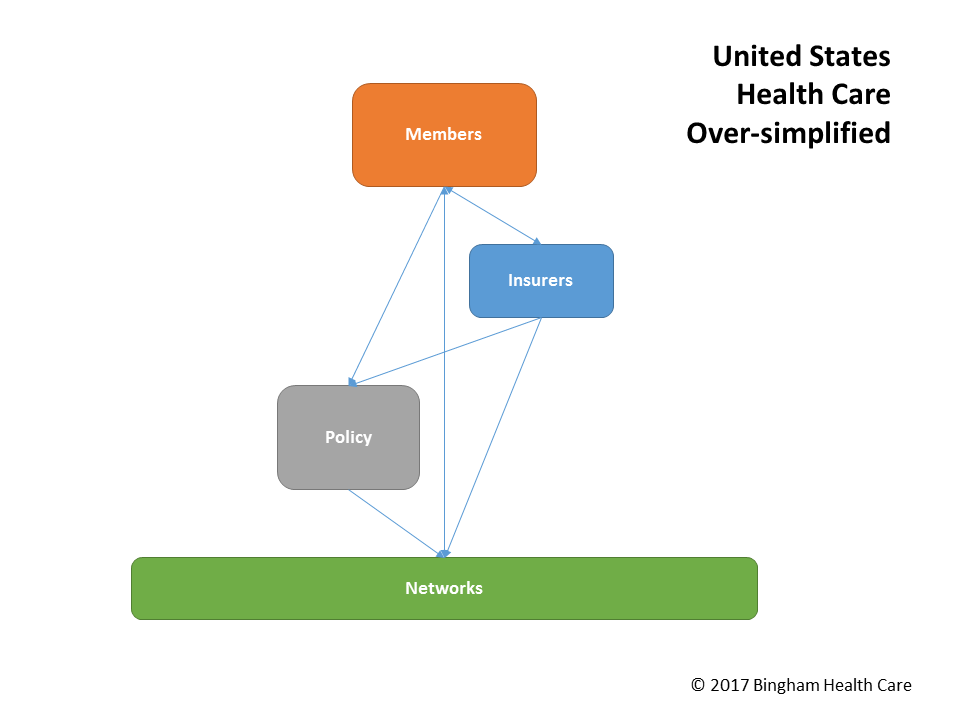

So that's it: a consumer (patient, member) buys a policy from a healthcare issuer (payer, insurer), then uses the policy to obtain care from healthcare providers (network) at favorable rates. The healthcare triangle and simple view depict these connections:

Let's briefly complicate the situation on three fronts: how does the issuer know how much to price the policy, what are ways the premium can be paid, and when a member gets care, what payments take place.

Pricing a policy so that the premiums sufficiently cover what the issuer will have to pay to providers when members get care under the policy, adding extra for uncertainty and profit, without going so high as to price the policy out of the market considering competing products. Issuers employ or contract with actuaries to help determine the best pricing range. Policy prices also have to pass regulatory approval and public review & comments. This is particularly important when an issuer decides to increase the price, as it potentially affects members on the policy when they wish to renew.

Commercial premiums are usually owed by the subscriber or contracted business, and premiums for public programs often are paid by the federal or state government. As long as the premium is paid in full, that obligation is satisfied, and the issuer is considered to have been made whole. To that end, some premium payments come from other members on the policy, besides the subscriber. They might even be paid by a member's family member, as a parent would do for his daughter. Also, commercial premiums come, in whole or part, from the Treasury, as subsidy payments. Another arrangement is that certain organizations—including the Ryan White Foundation—pay premiums for people meeting certain criteria, such as those with HIV or AIDS.

Premiums are paid up-front, regardless of whether or how much care is obtained under the policy. Sometimes arrangements with providers allow for capitated payments, on a per member per month (PMPM) basis, for the provider to give from zero to some level of care to each capitated member in exchange for this capitation. In other cases, or when care beyond capitated care is given, when care is actually provided to members/patients, providers are paid for this care. With healthcare coverage, some, most, or all of the provider payment is made by the issuer. However, many times there are also payments required of the patient. These frequently take the form of copayments or co-insurance, and can apply to the member's and/or family's deductible on the policy. As part of the contractual arrangement between the provider and issuer, detailed in a fee schedule, or by applying usual, reasonable, and customary charges, the amount the issuer pays to the provider is referred to as the allowed amount, although not infrequently providers bill the issuer (the billed amount) more than this. Note, too, that there are times that the provider gets what it can from the issuer, and bills the remaining or an additional amount to the member; this balance-billing practice may be prohibited in some cases.

Getting premium prices right is a critical decision process for payers, resulting in profit or loss and affecting brand & reputational image. Collecting premiums is also vital, in order to have sufficient cash on hand to pay for covered care. Finally, cost of care and member cost sharing are key parts of a delicate balance intended to attract customers, retain customers, maintain financial viability, manage member satisfaction, and develop a proper provider network. Please contact us for help optimizing your business operations, and obtaining or maintaining a competitive advantage.